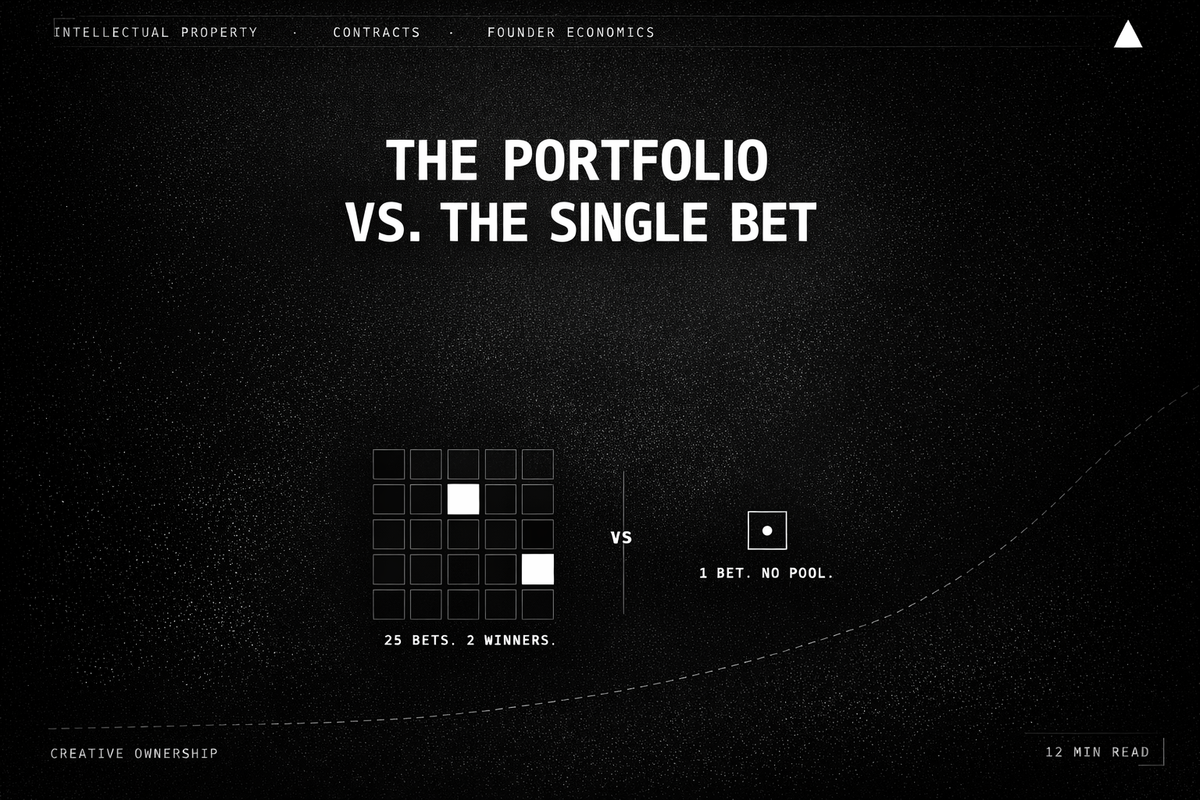

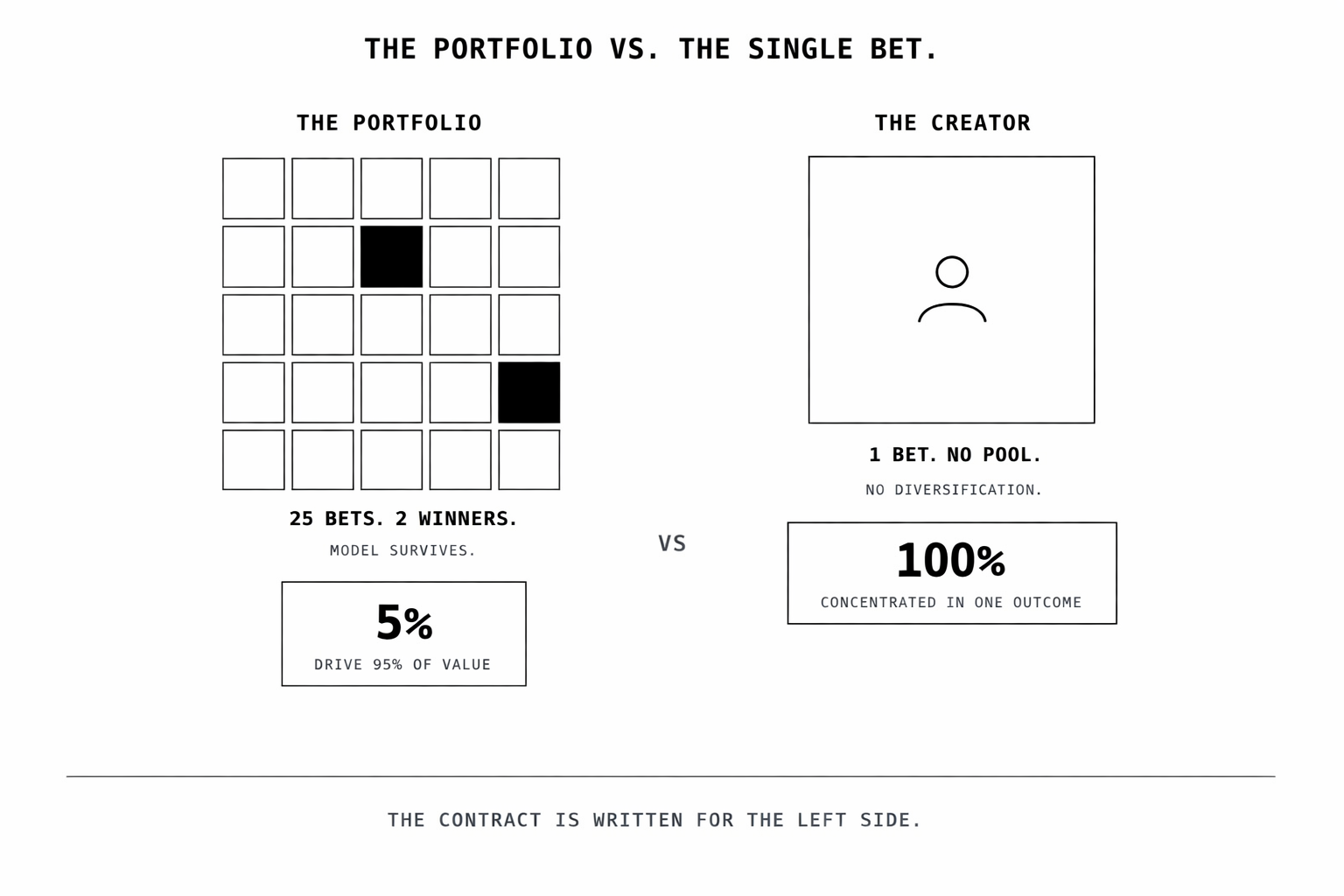

The Portfolio vs. The Single Bet

Why the Person Who Builds It Almost Never Owns It

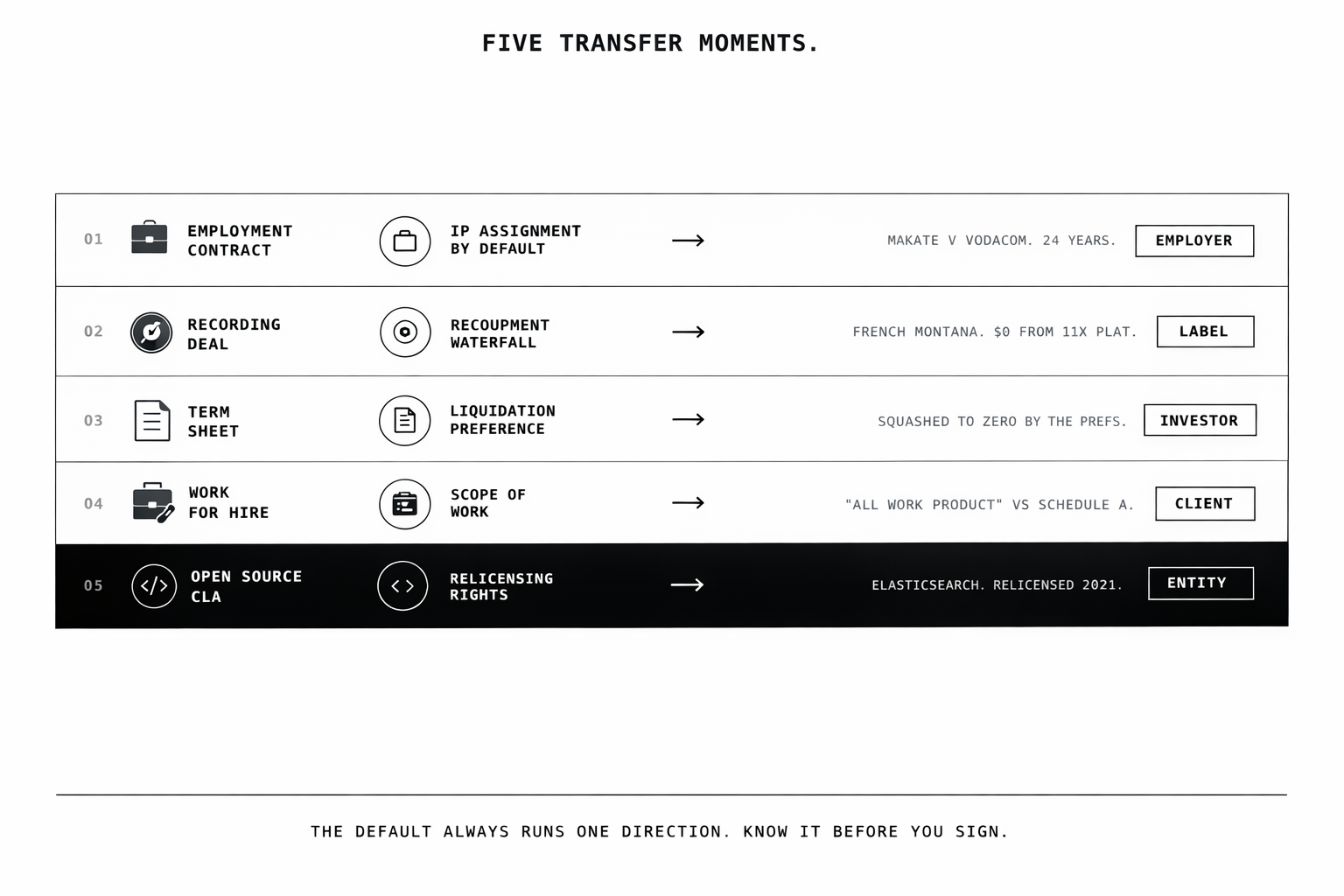

There is a moment in every recording contract negotiation where the artist's lawyer asks about the recoupment structure, and the label's lawyer explains it patiently, and the artist nods because they understand the words. Then they sign, because the alternative is going home without a deal. Six months later, when the single has 10 million streams and the royalty statement shows a negative balance, the artist finally understands what they agreed to. Not the words. The maths.

The same moment happens in a different room when a first-time founder signs a term sheet with a 1x participating liquidation preference and does not model what their 65% equity stake is actually worth under a realistic exit scenario. It happens when a developer signs an employment contract with an IP clause covering "all work product, whether created during or outside working hours, that relates to the company's business or anticipated business." It happens when a freelance designer signs a work-for-hire agreement that transfers copyright in perpetuity for a flat fee.

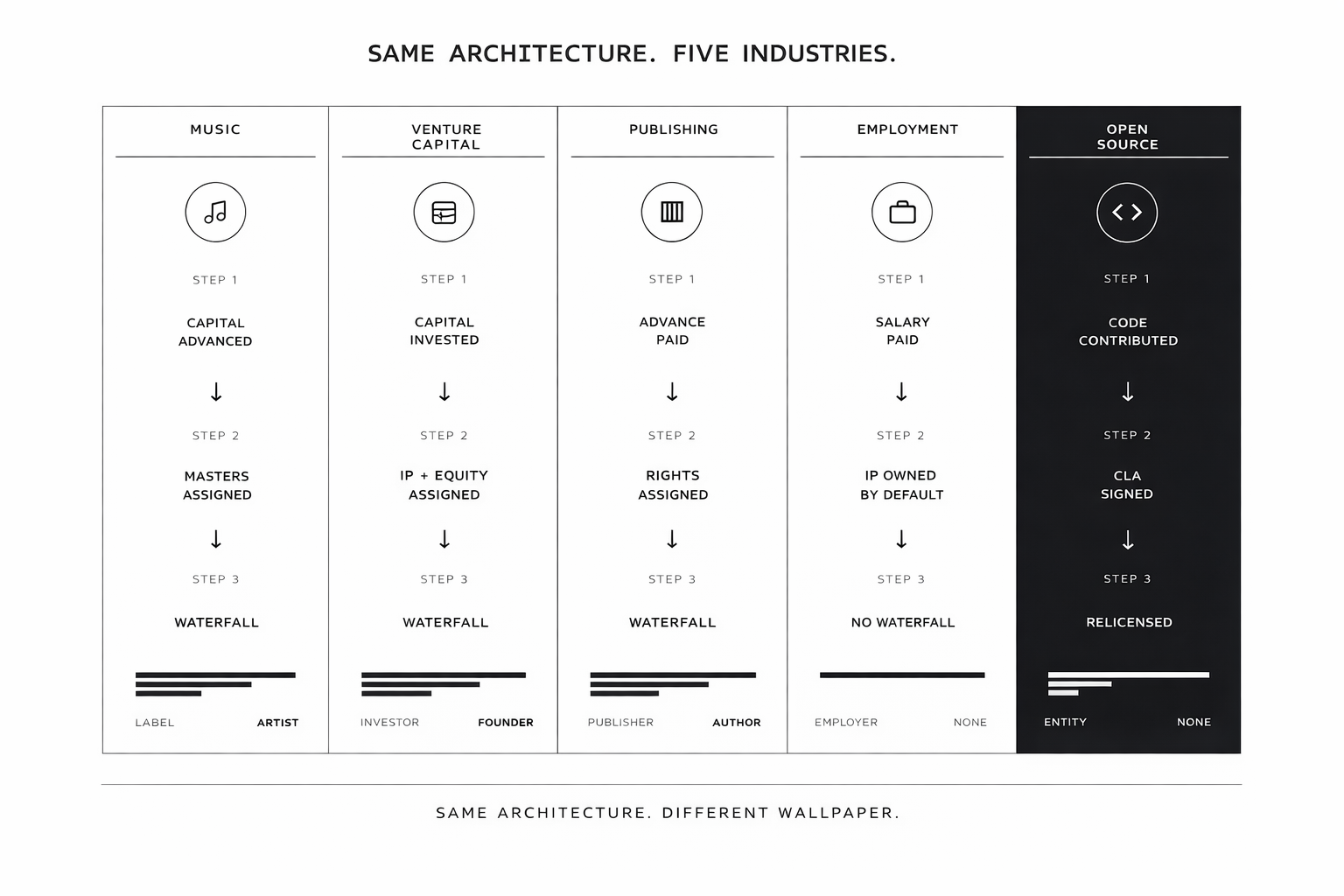

These are not the same industry. They are the same financial transaction, dressed in different clothes. And the first step toward navigating it is understanding that you are not dealing with a creative business. You are dealing with a financial one.

Every creative industry is a financial industry

A record label is a fund. So is a publishing house, a film studio, and a company that hires employees. They all do the same thing: pool capital, deploy it across a portfolio of uncertain bets, and structure the contracts so the rare winners compensate for the frequent losers.

This is not a metaphor. A bank's loan book is a portfolio. Individual borrowers default, but interest income from performing loans covers the losses. An insurance company pools premiums across thousands of policyholders, and the actuary's job is to ensure the pool absorbs individual claims without breaking. A private equity firm buys ten companies, restructures them, and knows that three or four exits need to carry the fund. A stock portfolio diversifies across uncorrelated positions so no single loss is fatal.

The creator, in every one of these industries, is the equivalent of a single loan, a single policy, a single stock. They cannot pool their own risk. That asymmetry is the entire game.

But here is the thing most creators miss: the portfolio model is not reserved for people with capital. It is a way of thinking, and creators can adopt it too. More on that shortly.

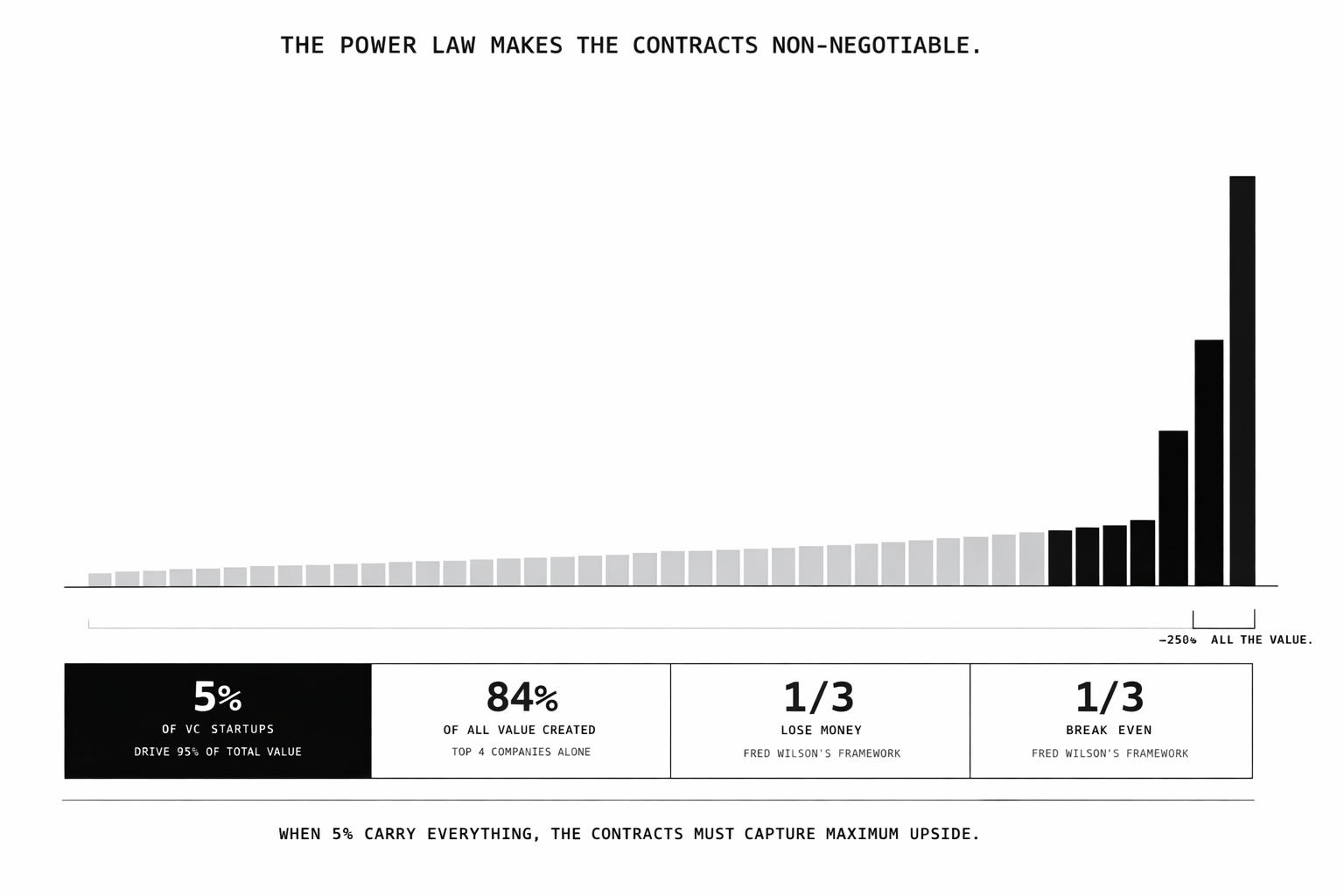

The power law makes the contracts non-negotiable

Fred Wilson, one of the most respected venture capitalists in the world, has described the maths plainly. An early-stage venture fund expects to lose money on a third of its investments, break even on another third, and generate real returns on only the final third. And within that top third, a single deal often needs to return a multiple of the entire fund to make the model work.

Y Combinator's data shows how extreme this gets. Across more than 5,000 funded startups, roughly 5% account for over 95% of the portfolio's total value. The top four companies alone, Airbnb, DoorDash, Coinbase, and Instacart, represent more than 84% of all market value created. Everything else is a rounding error.

This is the power law, and it is not unique to venture capital. Record labels see the same distribution: a handful of artists generate the revenue that sustains the entire roster. Publishing houses depend on a few bestsellers to fund hundreds of books that never earn out. Film studios greenlight thirty projects knowing three will be profitable.

When outcomes are this skewed, the portfolio entity has no choice. The contracts must capture maximum upside from the few bets that work, because nothing else covers the cost of the many that do not. Liquidation preferences, recoupment clauses, IP assignments, master rights transfers. These are not aggressive negotiating positions. They are survival mechanisms.

This is not something to fight. It is something to understand. The funder is not your adversary. They are running a model that requires certain protections to function, and without that model, most creative and intellectual work would not get funded at all. Your job is not to dismantle their model. It is to know it well enough to negotiate within it, and to build your own model alongside it.

The principal-agent problem shapes most of what you sign

The funder cannot sit in the studio, the office, or the codebase. They cannot observe effort, quality decisions, or honesty in real time. In economics, this is the principal-agent problem: the funder and the creator have misaligned incentives, and the funder cannot directly monitor behaviour. So the contract substitutes for observation.

This is why advances are structured as recoupable loans rather than gifts. If the label simply paid the artist and hoped for the best, the incentive to deliver would weaken. By making the artist's future income contingent on repaying the advance through royalties, the contract attempts to align effort with return.

It is why vesting schedules exist in startups. The investor cannot know whether the founder will still be committed in year three, so equity vests over four years with a cliff. It is why employment contracts assign IP by default: the employer pays a salary upfront and cannot verify that the output will justify the cost. Ownership of the work product is their hedge.

Most clauses in a creative contract can be understood through this lens. That does not make the clauses fair. It makes them predictable. And predictable means you can prepare.

The structural alternative to pure assignment is licensing. Instead of transferring ownership outright, you grant the funder a licence scoped to their specific needs: this product, this territory, this time period. They get what they are paying for. You retain the underlying IP. A consulting client does not need to own every framework you built to deliver their project. A publisher does not need world rights in perpetuity to sell your book in English. The default contract asks for everything because it is easier to draft and eliminates optionality risk. But a narrower grant, scoped precisely, often costs the funder nothing meaningful while preserving your ability to build on your own work in the future.

Asymmetric skin in the game

The combined effect of the power law and the principal-agent problem creates what Nassim Taleb calls asymmetric skin in the game.

The portfolio entity has limited downside. If one bet fails, the others absorb it. If the entire fund underperforms, the managers still collected fees. The structure is designed to make individual failure survivable.

The creator has the inverse. Years of their life invested in a single bet. Opportunity cost that compounds silently. Reputation attached to the outcome. And upside that is capped by a waterfall ensuring everyone else gets paid first. The risk is not shared. It is allocated, and it is allocated before the value exists, at the moment when the creator has the least information and the most need.

The structural response to this asymmetry is not to reject the deal. It is to rebalance the skin in the game where you can.

Revenue-share agreements do this directly. Instead of assigning IP in exchange for an advance, the creator retains ownership and the funder takes a percentage of revenue until a defined cap or multiple is hit. The funder still gets a return. The creator keeps the asset. This model is already common in indie film financing and is growing in music, particularly in the post-streaming era where artists are negotiating distribution deals rather than traditional recording contracts. In software, it shows up as revenue-based financing where the founder retains equity and the funder takes a percentage of monthly revenue until they have been repaid a multiple of their investment.

Reversion clauses are another mechanism. If the funder does not exploit the work within a defined period, the rights revert to the creator. These are standard in some publishing contracts and negotiable in music deals, though rarely offered by default. The creator gets a time-limited commitment rather than a permanent transfer. The funder loses nothing if they are actually using the work, and the creator does not end up with a permanently encumbered asset that nobody is doing anything with.

Taylor Swift's masters dispute made this dynamic globally visible. She signed with Big Machine Records at fifteen, and the deal gave the label ownership of her first six albums' master recordings. When Big Machine was sold to Scooter Braun's Ithaca Holdings for $330 million in 2019, Swift's masters transferred to a buyer she had no relationship with and no power to block. Rather than accept it, she re-recorded the albums under her new deal with Republic Records, where she owns her masters outright. The re-recorded versions outsold the originals. In 2025, she bought back the original masters from Shamrock Capital, finally owning her entire catalogue. The lesson is not that every creator can do what Swift did. She had extraordinary leverage. The lesson is that the structure of her original deal, standard for the industry, meant the most successful recording artist of her generation did not own her own work for nearly two decades. That is the default at work.

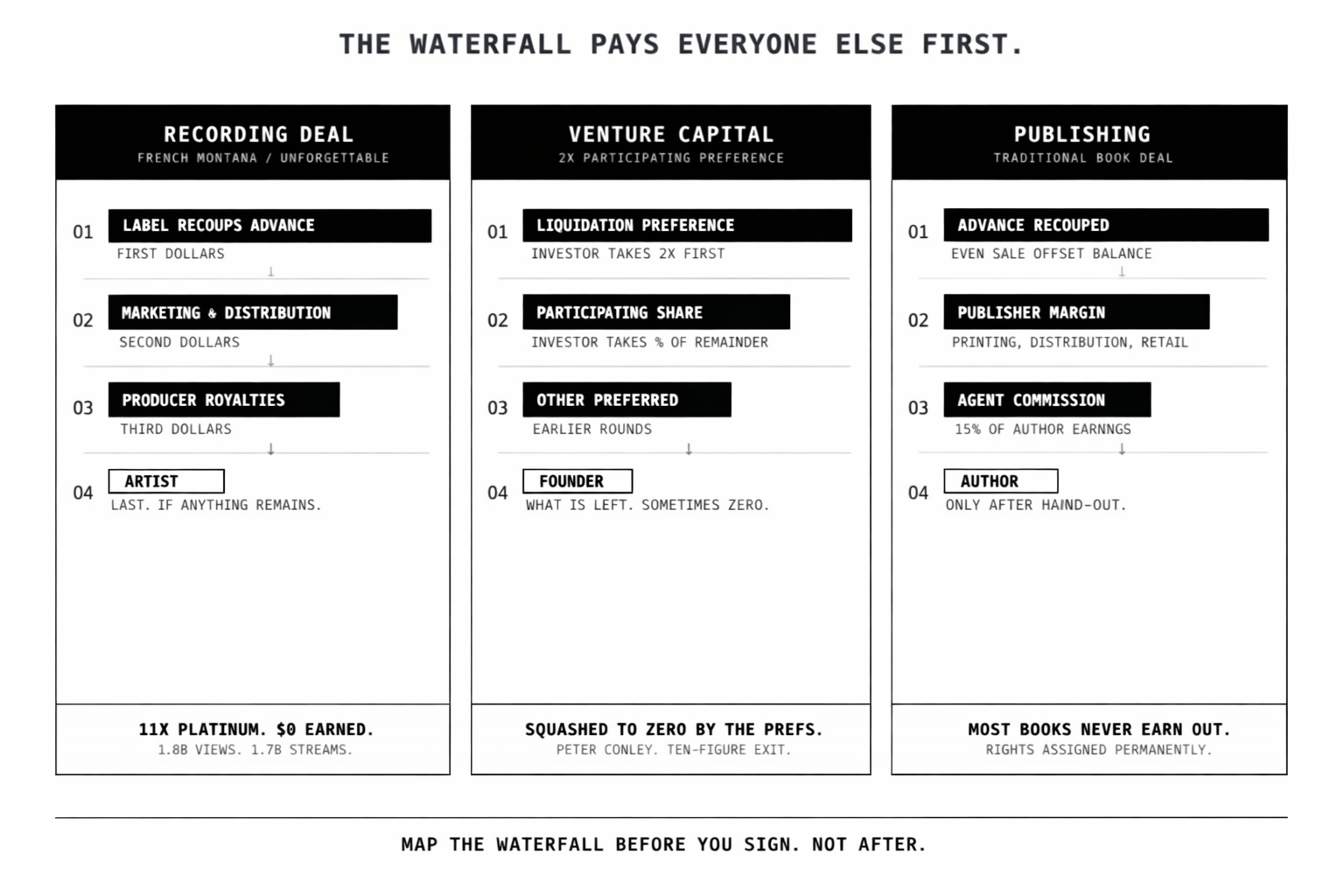

How the waterfall works

The waterfall is the sequence that determines who gets paid first when value is eventually created.

French Montana's "Unforgettable" makes this concrete. The song is certified 11x Platinum, with over 1.8 billion YouTube views and 1.7 billion Spotify streams. Montana spent $600,000 of his own money, $300,000 to clear the sample because Epic Records would not fund it, and another $300,000 to shoot the video in Uganda. He has said publicly that he has not made a dollar from the record. The biggest hit of his career, and the recoupment structure meant the revenue flowed to the label's portfolio first. The waterfall worked exactly as designed.

In venture capital, the waterfall runs through liquidation preferences. An investor with a 2x participating preference on a $5 million investment takes the first $10 million off the table in any exit, then participates again based on equity percentage. Angel investor Peter Cowley described a ten-figure exit in Cambridge where the founder, after a decade of building the company, was "squashed to zero by the prefs."

In publishing, the advance is the waterfall. The author assigns rights, and every book sold reduces the negative balance until earn-out. Most traditionally published books never reach that point.

In employment, there is no waterfall. The employer owns the output. The employee receives a salary. Full stop.

The lesson is not to avoid waterfalls. It is to map them before you sign. If you cannot draw the sequence on paper, showing who gets paid first, second, and last under your specific terms, you do not understand the deal you are entering.

The five transfer moments...